The African Shopper and The Cart They Cannot Check Out

Africa’s consumers are watching the world’s biggest retail moment from the outside. With $96 billion in diaspora remittances, a $2 trillion household economy, and 350 million middle-class shoppers hungry for global brands, the demand is real. The access is not. A new wave of retail aggregators is changing that. It is 11:58 p.m. on the […] The post The African Shopper and The Cart They Cannot Check Out appeared first on Time Africa.

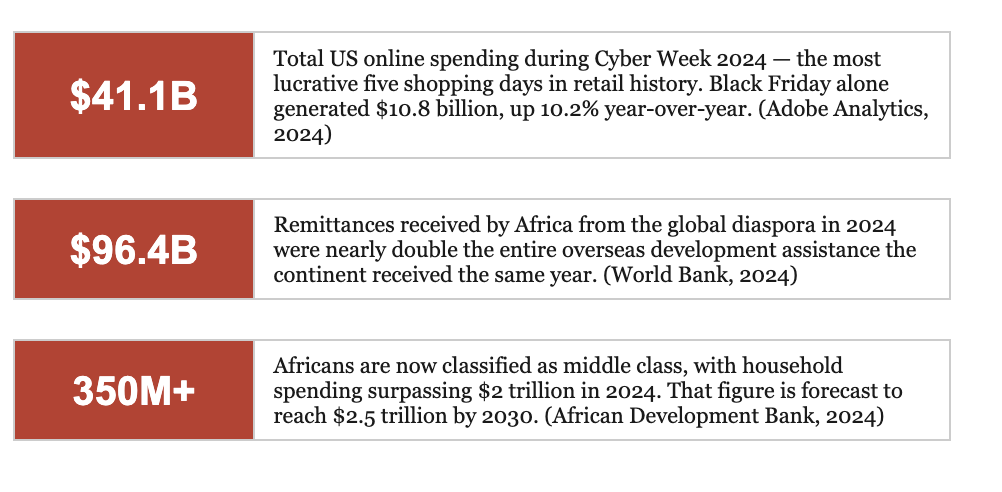

Africa’s consumers are watching the world’s biggest retail moment from the outside. With $96 billion in diaspora remittances, a $2 trillion household economy, and 350 million middle-class shoppers hungry for global brands, the demand is real. The access is not. A new wave of retail aggregators is changing that.

It is 11:58 p.m. on the last Friday of November. In a high-rise apartment in Houston, Texas, Abena, a 31-year-old Ghanaian nurse, has three browser tabs open simultaneously: Amazon, Sephora, and the Nike SNKRS app. She has been waiting for this moment for weeks. The Charlotte Tilbury Hollywood Flawless Filter she has tracked since September has just dropped to $32. The Air Jordan 1s that her younger brother, back in Accra, has been begging for are finally at a price she can justify. Her cart is full. Her card is ready, but Abena is not shopping for herself alone. She is shopping for home.

Scenes like this play out across millions of households in the African diaspora every Black Friday, a quiet, distributed shopping ritual that official retail data has never fully captured. These are consumers who know the global market intimately, who track US prices with the discipline of day traders, and who navigate the gap between American abundance and African access with a mix of ingenuity, trusted contacts, and sheer determination.

That gap between what Africa’s consumers want and what global retail actually offers them is the defining logistics story of the decade. And it is being solved, one shipment at a time.

The world’s biggest shopping event has a geography problem. Black Friday has become a global cultural phenomenon. South African shoppers spent over R3.2 billion during Black Friday 2024, with beauty product sales running 125% above an average Friday, and 67% of all transactions completed on a mobile phone. Across Nigeria, Ghana, Kenya, and beyond, social media feeds flood with countdown timers and wishlist posts every November.

The appetite is not in question. But the appetite is almost entirely disconnected from the source.

Nike USA does not ship to Ghana. Sephora’s checkout does not recognize a Ghanaian or Nigerian billing address. Amazon’s global shipping program covers a fraction of its catalog, typically excluding the most in-demand items. Best Buy does not ship outside the United States at all. The brands that dominate African consumers’ wishlists have, for the most part, built their logistics infrastructure around markets they could see clearly: North America, Europe, and parts of Asia. Africa has been an afterthought, if it registered at all.

The result is a peculiar consumer paradox: one of the world’s fastest-growing consumer markets with a youth population that is more brand-conscious, more digitally native, and more globally connected than any previous generation is systematically locked out of the global retail moment it has fully bought into, culturally and aspirationally.

Africa is not a market that lacks consumers. It is a market that lacks infrastructure, the invisible bridges between demand and supply that the rest of the world takes for granted.

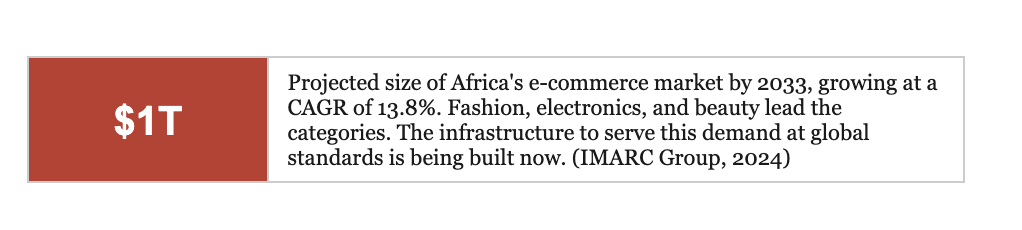

Africa’s e-commerce market generated $317 billion in 2024 and is projected to cross $1 trillion by 2033, growing at a compound annual rate of nearly 14%. Fashion and clothing represent the single largest category, accounting for 24.4% of total e-commerce revenue in 2024, with online fashion sales projected to hit $13.4 billion by 2025. Electronics follow closely with $11.2 billion in annual online sales by 2025, driven by an insatiable appetite for authentic, competitively priced devices that rarely reach African retail shelves at fair value.

Nigeria alone accounts for 26% of Africa’s entire e-commerce market. Ghana’s remittance receipts surged 91% in 2024 to reach $4.6 billion, which flows directly into households where consumption decisions about brand-name goods, electronics, and quality provisions are made daily. Nigeria received $19.8 billion in diaspora remittances the same year, representing 35% of all sub-Saharan Africa’s inflows. These are not small economies of aspiration. These are vast, liquid consumer markets that global retail has been slow to serve.

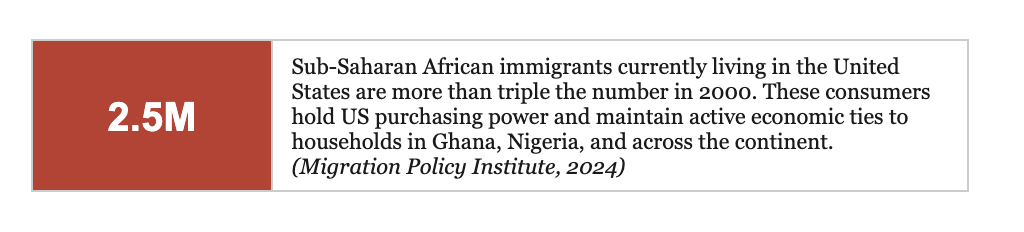

The diaspora amplifies everything. Approximately 2.5 million sub-Saharan African immigrants live in the United States today, more than triple the number recorded in 2000. Among them are roughly 905,000 Nigerians, 332,000 Ghanaians, with significant communities from Ethiopia, Kenya, and South Africa. These are educated, professionally employed consumers with US purchasing power and deep, active ties to family at home. They are not occasional gift-senders. They are systematic provisioners, sourcing everything from school supplies to electronics to barrels of non-perishable groceries for households that depend on them.

Africa’s logistics landscape is, to borrow from the industry’s own vocabulary, fragmented. The continent spans 54 countries, dozens of distinct customs regimes, multiple currency zones, and infrastructure quality that varies from world-class port facilities in Lagos to unpaved final-mile roads in secondary cities. Cross-border regulatory fragmentation drives up administrative costs and delays. Fuel volatility destabilizes long-haul trucking economics. Customs documentation requirements can double the effective transit time of a shipment.

But the fragmentation that most directly affects the average consumer is less visible than a customs queue. It is structural: the absence of a trusted, accessible, end-to-end pathway between a shopper in Accra and a shelf in an American store.

The informal workarounds have always existed. Travelers carrying goods in checked luggage. Diaspora relatives are building second-hand shipping networks through church groups and community associations. WhatsApp groups where people pool orders and share the cost of a reliable contact who happens to be flying home next month. These systems work until they don’t. They are built on personal trust, not scalable infrastructure. They cannot process 5,000 orders during a Black Friday sale. They cannot offer guaranteed delivery timelines or insurance. They cannot generate an invoice denominated in cedis.

What the market has been waiting for is the formalization of the conversion of these informal trust networks into dependable, transparent, scalable service infrastructure.

The demand was never the problem. A Ghanaian mother in Kumasi has known exactly what she wants from Costco for years. The problem has always been the bridge.

A new category of operator is emerging to solve the access problem at its root: the retail aggregator. Rather than trying to change how Amazon or Nike approach African markets, a generational project, retail aggregators work within the existing US retail infrastructure, acting as licensed, trusted buyers on behalf of African consumers. The model is elegant in its simplicity: you identify the product, the aggregator buys it at the US price, consolidates it with other orders where possible, and ships it directly to your door.

It is personal shopping at scale. And it is beginning to formalize what was previously an entirely informal economy.

ShipEasy (www.justshipeasy.com), a logistics and commerce startup founded by a Ghanaian diasporan, represents this model in action. Based in the Washington D.C. area, the service buys directly from Amazon, Sephora, Nike, Best Buy, IKEA, AutoZone, Costco, Walmart, and BJ’s Wholesale Club, the full breadth of mainstream American retail, and ships to Ghana and Nigeria via both Express (three to five business days) and Standard (five to eight weeks) services. The pricing model is transparent: a fixed percentage markup on the item cost, variable pricing based on items for standard shipping, and a flat per-kilogram rate for express air freight.

What distinguishes this approach from informal courier networks is not just the speed or the formality but the range. ShipEasy ships everything: skincare palettes and limited-edition sneakers; PlayStation 5 consoles and Bose sound systems; IKEA bedroom furniture, cars, and AutoZone car parts; bulk Costco provisions; olive oil, cereal, baby formula, and cleaning supplies packed into a single barrel for a flat shipping fee. The service does not specialize in one category because African consumers do not limit themselves to one category. They want access to the whole store. This is the retail aggregation thesis.

There is perhaps no more eloquent expression of the demand ShipEasy serves than the barrel, the humble, blue plastic drum that has been the defining object of Caribbean and African diaspora shipping culture for half a century. For generations, families have filled barrels with goods unavailable or prohibitively expensive at home: corned beef, cooking oil, toiletries, baby formula, medicines, fabrics. A filled barrel is a care package, a provision store, and an act of love compressed into 55 gallons.

ShipEasy’s Fill the Barrel service takes this tradition and brings it into the formal economy: a flat fee, a scheduled shipping date, a packing list built from Costco, Walmart, or BJ’s, and a tracked delivery to the customer’s door. Groups of siblings, church communities, or extended families pool their items into a single barrel and split the cost. One flat fee. One tracked shipment. No guessing at what the final cost will be.

It is an ancient practice made reliable. And it points toward a broader truth about how African logistics will develop in the next decade: not by replacing informal community networks, but by formalizing and amplifying them.

The barrel is not a relic. It is a prototype. It tells you exactly what the consumer wants: access, trust, value, and a known price before the goods leave the shelf.

The macro indicators are uniformly bullish. Africa’s freight logistics market is forecast to grow at a CAGR of 6.4% through 2034. The African Continental Free Trade Area, fully operational since 2021, is steadily reducing intra-African trade barriers. Mobile penetration has crossed 50% on the continent, and over 73% of e-commerce transactions are now completed on mobile devices. The infrastructure of digital commerce, payments, identity verification, and last-mile delivery is maturing faster than any comparable market in history.

What has lagged is the bridge layer: the operators who sit between global retail and African consumers, translating availability into access. That layer is now being built, in part by large logistics conglomerates and, perhaps more importantly, in part by nimble, community-rooted operators who understand the specific texture of diaspora demand.

The opportunity for African governments, port authorities, and trade regulators is to accelerate this process: streamlining customs documentation for low-value personal imports, enabling real-time package tracking integration with national postal systems, and reducing the cost of inbound international air freight, currently among the highest in the world on a per-kilogram basis. Every percentage point reduction in friction at the border translates directly into lower prices for the end consumer and greater competitiveness for African-owned logistics operators.

The private sector, meanwhile, has already voted with its operations. The emergence of services like ShipEasy is not a niche phenomenon. It is an early signal of a structural shift, the beginning of Africa’s formal integration into the global retail supply chain from the demand side, driven not by multinational investment but by the purchasing power of its own diaspora.

From the Wishlist to the Doorstep

Back in Houston, Abena finishes her checkout just before midnight. The Charlotte Tilbury filter. The Jordans for her brother. A few items from Costco, oats, canned fish, the big bottle of olive oil her mother has been asking for. She types the order details into a WhatsApp message and hits send. By morning, a quote arrives in her preferred currency. By next week, the items will be purchased, consolidated, and en route.

The distance between an American shelf and an African doorstep has not changed. What is changing is the infrastructure that spans it and the growing ecosystem of operators determined to make that span feel, for the first time, effortless.

Africa’s consumers are not waiting for global retail to discover them. They are building their own front door.

The post The African Shopper and The Cart They Cannot Check Out appeared first on Time Africa.